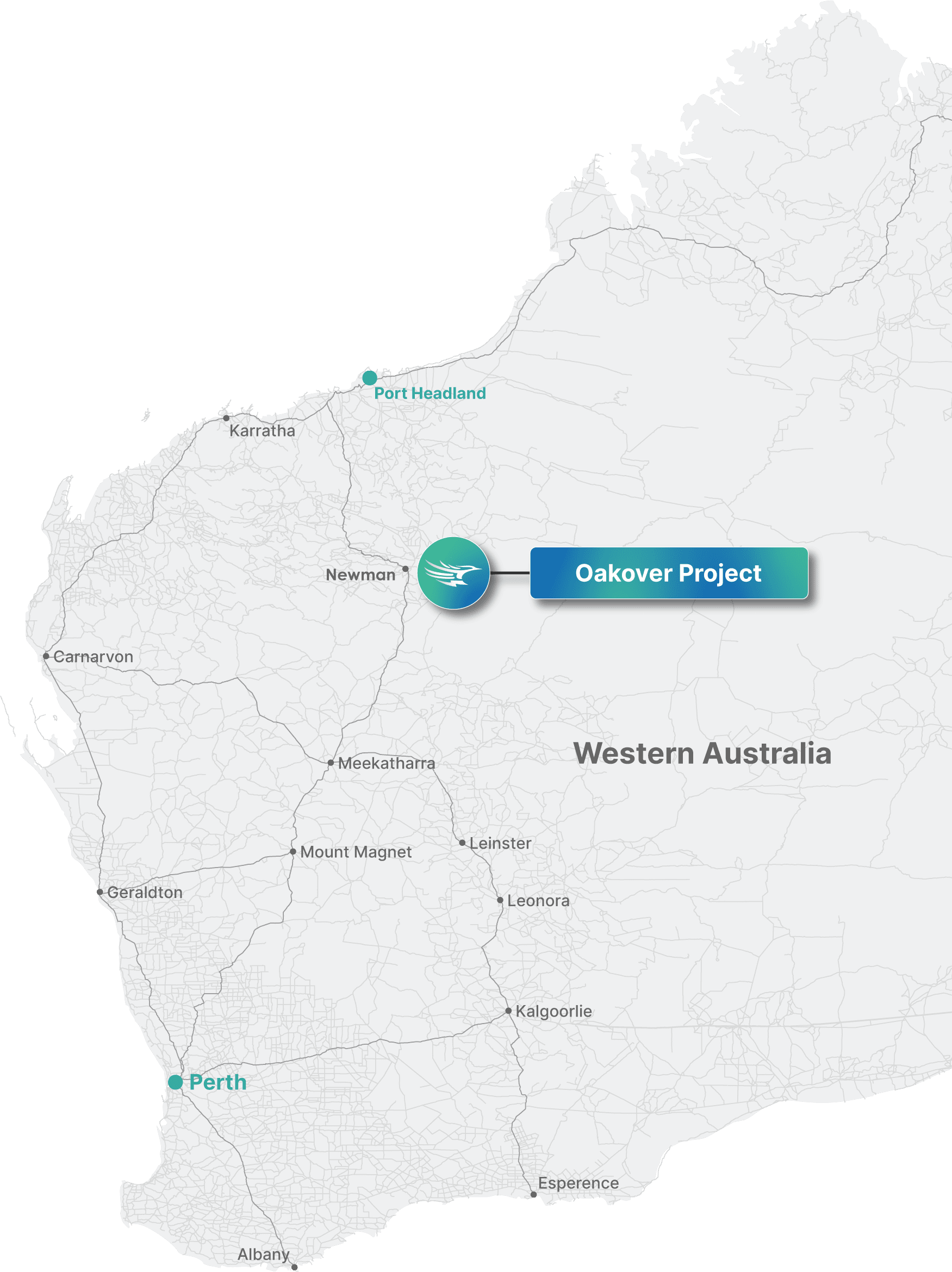

A Strategic Resource Securing Long-Term Manganese Supply for our Battery Materials

Oakover provides the future upstream security for our manganese chemicals business, with favourable geology, near-surface deposits and metallurgical testing confirming battery-grade material viability.

- Resource: 176.65 Mt @ 9.9% Mn

- Project Value: A$741.3 M NPV

- Return on Investment: 73.1% IRR

- Project Lifespan: 18-year Life of Mine

- Fully Permitted

Mineral Resource Estimate

| Mineral Resource Classification |

Tonnes (Mt) |

Mn (%) |

Fe (%) |

SiO₂ (%) |

Al₂O₃ (%) |

P (%) |

| Indicated | 105.78 | 10.1 | 8.9 | 39.2 | 9.8 | 0.10 |

| Inferred | 70.87 | 9.6 | 8 | 36.5 | 9.5 | 0.09 |

| Total | 176.65 | 9.9 | 8.6 | 38.1 | 9.7 | 0.10 |

Related ASX Announcements

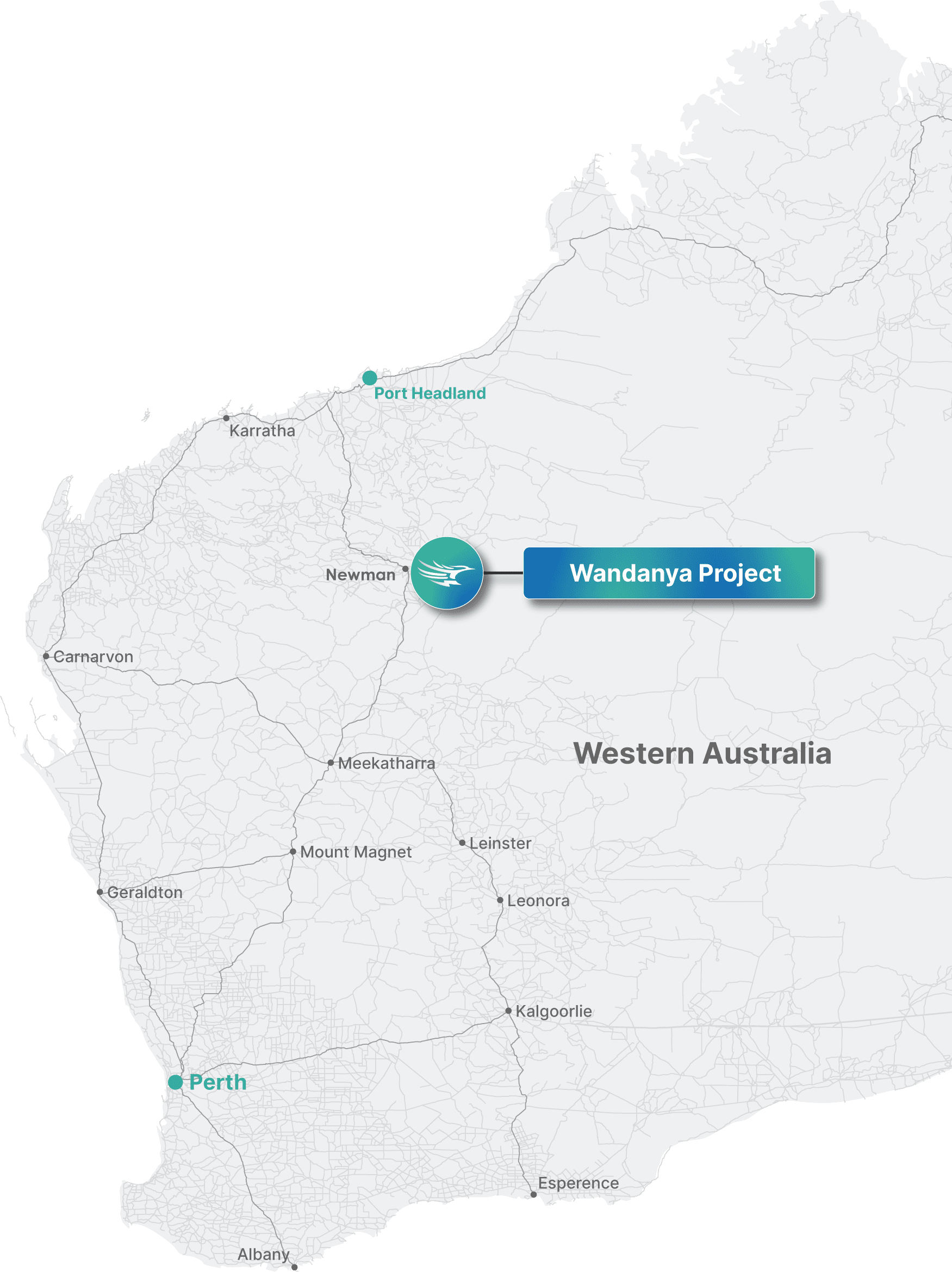

Wandayna Project

A High-Grade DSO Exploration Opportunity Near a World-Class Manganese Operation

Wandanya offers near-term exploration upside in the Eastern Pilbara, supported by strong historical results and a clear farm-out funded drilling pathway.

- Tenure: E46/1456 & E46/1457 (ELA)

- Project Area: 51 km²

- Historical Drilling: 113 holes for 1,975m

- Grade Highlights: Up to 40.8% Mn intercepts; rock chips up to 64.96% Mn

- Farm-Out Funding: $112,500 (12 months) to earn 80% + minimum RC drilling program